Nothing discussed/written should be considered as investment advice. Please do your own research or speak to a financial advisor before putting a dime of your money into these crazy markets. In other words, if you buy something I bought, you deserve to lose your money.

The only reason why I am making my portfolio public because it provides accountability to me. Some or all the analysis I provide could befrom the top of my head and should not be considered accurate.

My investing goal is simple; to try to manage risk while being fully invested without market timing. Howard Marks said it best, “even though we can’t predict, we can prepare.”

All my references to the Market are only for the US Market.

Performance

YTD I am up 17% versus 14% for the SP 500.

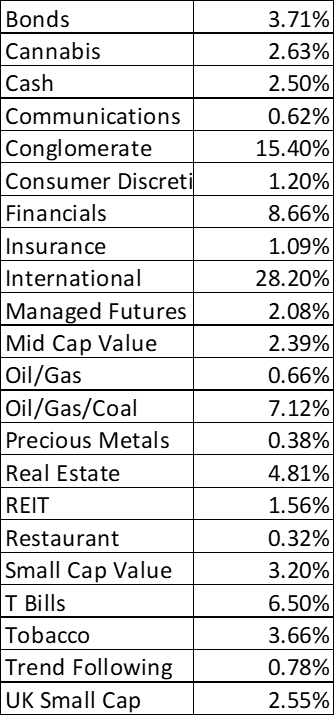

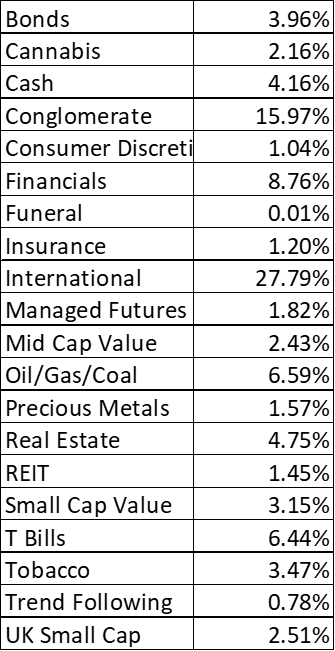

The table below is a breakdown of my portfolio at the end of Q3. What you see below where my entire net worth, excluding my home, is allocated.

Portfolio Activity

Opened a position in Charter (CHTR). The company is essentially an internet and mobile phone business. There probably won’t be a lot of organic growth but its trading at 5.5 earnings but its buying back its shares. Since 2020 they have bought back 29.5% of its shares and since last year 3.77% shares were repurchased. If they make $50 per share and if the multiple increases to 10 then the stock is worth $500.

I opened a small position in United Healthcare (UNH). After doing some digging and after a 30% increase I exited my position. During my reading I got vibes of GE; a company so big that I don’t think I would understand all the moving parts enough to feel like I understand the business. I know a lot of smart people have bought the stock but I had to exit.

I opened a position in Portillos (PTLO). I’ve never eaten there but the data looks amazing. In March of this year they launched their Loyalty Rewards Program and they already have 1.9 million people signed up. They operate 94 restaurants which means on a per restaurant basis they have more than 20,000 loyalty members. To put this into context, Chipotle has 40 million loyalty members across 3,700 locations which averages out to 10,000 loyalty members per restaurant. Portillo’s has double the number of Chipotle. In 2014 a private equity firm bought Portillos for $1 billion. Today the company has a market cap of $509 million.

The value investor bias can’t help but get excited about banks trading for less than their book value. Bankfirst Corp (BFCC) is trading at about 60% of book value. Management authorized a $10 million dollar buyback (about 4% of its market cap) and has already purchased 21,909 shares for $785,000 (average price of $35.83). Non-performing assets to total assets of 0.51% as of March 31, 2025 compared to 0.42% March 31, 2024.

I exited my position in Seaport Entertainment Group (SEG) at 34.6% profit. The company fired the CEO and CFO with additional changes to the board. Part of my thesis was the CEO and his successful history. I’ll continue to follow the company but I am out.

I opened a position in Olin Corporation (OLN). The company is manufacturer and distributor of chemical products and a leading U.S. manufacturer of ammunition (Winchester). They produce a myriad of chemical products such as chlorine, ethylene dichloride, hydrochloric acid and allylics. The stock is down 53% in one year due to cyclicality nature of their business. Additionally, Winchester is the largest ammunition maker in the US (to individuals and the US Army and government). Despite this company still pays a dividend and has a 8% free cash flow yield and the company is buying back stock. Lastly, the first debt maturities doesn’t begin until 2029.

I opened a position in Crocs (CROX). I personally had a bias against their product because I would never buy their shoes. However, I cannot deny the popularity of their shoes. The company has a market cap of $4.4 billion and an enterprise value of $5.8 billion along with a free cash flow yield of $750 million. On top management is buying back their stock; YTD they’ve bought back $580 million. The brand recently said sales grew 30% in China which is amazing for an American company. With fashion the shelf life of a product could evaporate very quickly but at the price I paid I think on a risk-reward basis it is a bet worth making.

Quotes & Charts

“We avoid doing simple things that work because they don’t make us look smart.”

“Smart people feel stupid doing simple things, so we invent complicated alternatives that accomplish less but feel more intellectually satisfying.”

“Meanwhile, the people who dominate their fields are doing embarrassingly basic things, but they do them better than everyone else.”

“The 2021-2023 inflation was fundamentally fiscal in origin, caused by massive spending without credible repayment plans rather than monetary policy or supply shocks.”

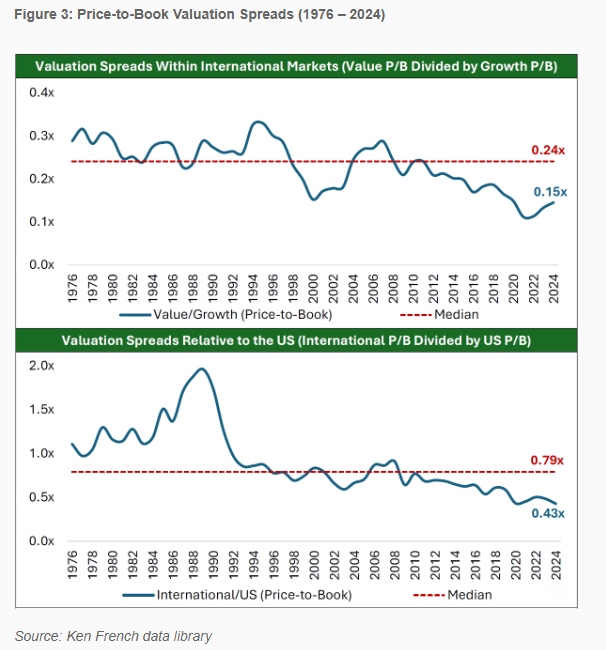

“This means that there are at least two potential upside levers for international value stocks going forward. In addition to mean reversion of valuation spreads within international markets, we also believe there is an upside opportunity from narrowing the valuation discount between international markets and the US. We believe that the combination of these two discounts—particularly among small- and micro-cap firms—offers one of the most attractive setups in global equities today.”

When I came in third I had 88 points, which is close to the 90 points I target every year. That said, 88 points surely enough to win a lot of times.

So what happened? Basically I was the 2025 Mets in that I started off extremely strong but my pitching fell apart via through injuries, bad luck or me just having a poor projection system.

My pitching was strategy was to draft elite closers and supplement them with good, but not great, starting pitchers. Edwin Diaz and Josh Hader were both top 7 relievers but Mason Miller and Jeff Hoffman underperformed. In my analysis I thought there was no way Miller would be traded because I thought the A’s had a sneaky opportunity to make a playoff run.

Injuries played big role. Hunter Greene only pitched 100 innings; Pablo Lopez 75 innings; Tylor Megill 68 innings; Nestor Cortes 34 innings and Justin Steele 34 innings. I was counting on these guys to be my #1 and #2 starters.

Poor evaluation also played a big role. I projected a 3.60 ERA for Sonny Gray and he finished with 4.28 ERA (with a 3.29 SIERRA). I projected Brandon Pfaadt as a top 40 pitcher and he ended being worth -$8. I drafted Mitch Keller to be a streamer at home…well, his numbers were worse at home. The best pitching staff I had was when I drafted three #2 starters in Carlos Rodon, Sonny Gray and Pablo Lopez. I think this is a strategy I’ll have go with moving forward so I can have more pitching depth.

Nothing discussed/written should be considered as investment advice. Please do your own research or speak to a financial advisor before putting a dime of your money into these crazy markets. In other words, if you buy something I bought, you deserve to lose your money.

The only reason why I am making my portfolio public because it provides accountability to me. Some or all the analysis I provide could befrom the top of my head and should not be considered accurate.

My investing goal is simple; to try to manage risk while being fully invested without market timing. Howard Marks said it best, “even though we can’t predict, we can prepare.”

All my references to the Market are only for the US Market.

Performance

YTD I’m up 9.30% compared to 5.18% for the S&P 500 (without dividends reinvested).

The table below is a breakdown of my portfolio at the end of Q2. What you see below where my entire net worth, excluding my home, is allocated.

Portfolio Activity

I exited my positions in Marcus Corp and ETSY because I wanted allocate funds to Alexandria Real Estate (ARE). Alexandria is a life science REIT. They owner, operator, and develop Megacampus’ in Greater Boston, the San Francisco Bay Area, San Diego, Seattle, Maryland, Research Triangle, and New York City. YTD the stock is down 24.75% and is down 45% from its all-time highs. I think the stock price is being punished due to the sector they are in is hated and there is uncertainty with the NIH funding cuts and the FDA broadly. The company has a 7.8% dividend without much debt and the average remaining debt has a term of 12 years. In Q1 they reported that occupancy was at 91.7%, which was down 2.9% from the prior quarter. About two thirds of the decline was related to the 768,000 square feet of lease expirations across four submarkets. The remaining one third represents several smaller spaces spread across multiple markets, of which the two largest spaces in that bucket have been re-leased and are expected to be delivered later in 2025. Management is reducing debt and is buying back stock. In the last six months the company has bought back 1.6% of its shares at an average price of about $97. In three weeks they will release earnings and I suspect more shares to have been repurchased.

Thrift Update

I wrote about CFSB Bancorp (CFSB) a year ago and the bank is being acquired by Hometown Financial Group for $44 million, $14.25 per share which is more than double what I paid. As of this writing the stock price is $13.70. It was trading at 58% book value when I bought it last year. The deal will close in Q4 2025. I’m going to keep my shares until the acquisition closes.

William Penn Bancorporation (WMPN) was acquired for $11.40 per share ($127 million). I only made about 6% on this investment. It was trading at 89% of book value when I increased my stake in the company.

NorthEast Community Bancorp’s (NECB) stock price hasn’t changed very much since I increased my stake last year. It’s still trading a book value. The ROEs the past two years have been 17 and 16% respectively. The company has not engaged in buybacks, which kinda stinks because the stock has a PE of 7.50 while a lot of well run banks are trading at a PE of 10. In January the stock had a high of $31.72. The five year average ROE is 11.36%, which is really good.

Cullman Savings Bank (CULL) is up about 9.5% since my purchase last year. The bank is trading at 69% of book value and the company has purchased roughly 8.5% of its stock. The stock appears to be really cheap. In the last two years they have repurchased 10.5% of its stock at a $10.50 price.

PB Bankshares Inc (PBBK) trades at 83% of book value. Book value per share is $19.40 and the stock is trading at $16.10. The company has bought back 5.2% of its shares since March 2024 at an average price of $13.25. The company had its Standard conversion four years ago so its possible they will get acquired sooner rather than later (hopefully).

Bogota Financial Corp (BSBK) is trading roughly the same as when I bought it last year ($7.28), but it did have a high of $8.66 this past September. They repurchased 0.85% of its stock at a price of $7.14. ROE was -1.6% in 2025 and only 0.50% in 2023. The stock is trading at 68.50% of book value but if the company isn’t profitable then it’s time to move on.

In April 2024 First Seacoast Bancorp (FSEA) announced a share repurchase of 507,707 shares of common stock, representing approximately 10% of the then outstanding shares. To date, the company has repurchased 397,008 shares at an average price of $9.15 per share. In December 2024 the company announced an additional repurchase authorization of approximately 5% of shares. Two weeks ago the company announced a CEO transition. The company has had three years of negative ROE so it is time to sell.

BV Financial Inc (BVFL) is relatively flat since my purchase last year but a lot of good things have been happening underneath the hood. The company announced a share buyback in July 2024 for 10% of the shares, which was completed in January 2025 at an average price of $17.06. This past April the company announced another repurchase program for up to 10% of the shares. The stock is trading at 78% of book value and its average ROE the past five years is 9.92%. Also, non-performing assets has steadily decreased.

Ponce Financial Group Inc (PDLB) is trading at less of a discount than a year ago. That said, stock is very cheap because it’s currently trading at 65% of book value. It is very odd that management has not allocated any capital to share repurchases. They had their second conversion three years ago and they’re no longer restricted to do repurchases. In the last five years the company has an average ROE of 2.2%, which is below average, even for thrifts. That said, the price is too cheap; I will add a little.

Columbia Financial Inc (CLBK) continues to trade at a premium to book value despite the average ROE of 5%. I will continue to hold but this bank is in the too hard pile.

FFBW Inc (FFBW) is up about 7.5% since last year. They started repurchasing shares in 2023 buying back roughly 8% but the share count increased slightly this past year. The company is trading at 88% of book value and ROEs are steady in the low-to-mid 2%’s. This is a hold.

Magnolia Bancorp Inc (MGNO) is a Standard conversion that occurred in January 2025. It is currently trading at 46% of book value and it has a market cap $9.2 million. Total non-performing assets as a percentage of total assets is only 0.09%. It is not uncommon for banks to have an IPO with no earnings or to be losing money so I am going to overlook the low ROEs. About 48% of their deposits are CDs which isn’t great either. All that said, the price is too cheap to not start a small position.

Monroe Federal Bancorp (MFBI) is a Standard conversion that occurred in October 2024. The company reported a net loss of $322,000 for the nine months ended December 31, 2024, a $328,000 decrease from net income of $6,000 the nine months ended December 31, 2023. The stock price is up 26% since it went public and it’s only trading at 75% of book value but this is a wait and see because I do not believe I am getting a big enough margin of safety.

FB Bancorp (FBLA) is a Standard conversion that occurred in October 2024. It is currently trading at 68% of book value. The equity to assets has averaged about 15% the past two years. Total non-performing assets to total assets the past two years have averaged less than one percent. Deposit quality looks good. I’ll start a starter position.

EWSB Bancorp (EWSB) is a Standard conversion that occurred in September 2024. It is currently trading at 46% of book value. Total non-performing assets to total assets the past two years have averaged 0.06%. The equity to assets was 5.7% in 2024 which is a little concerning. I typically look for this to be greater than 12%. Also, non-time deposits are only about 52% of deposits. The price is very cheap so I’ll take a small position and monitor.

The equity to assets has averaged about 15% the past two years. Deposit quality looks good. I’ll start a starter position.

Fifth District Bancorp (FDSB) is a Standard conversion that occurred in August 2024. It is currently trading at 54% of book value and its equity to assets was 24% last year. 61% of its deposits are CDs which isn’t preferable, but 90% of their loans are family home mortgages…of which most of them have flat rate mortgages. Non-performing assets were roughly 0.22% on average the past two years.

NB Bancorp (NBBK) is a Standard conversion that occurred in December 2023. It is currently trading at 91% of book value. Equity to assets is 14.8% and non-performing assets were only 0.26% the past two years but CDs represent 58% of their deposits. This is a buy a small amount and continue to monitor.

Gouverneur Bancorp (GOVB) is a Second conversion that occurred in November 2023. It is currently trading at 45% of book value. Equity to assets have averaged about 12% the past two years; CDs are only 23% of deposits and most of their loans are for residential home mortgages. In December 2024 they announced at 5% buyback.

Central Plains Bancshares, Inc. (CPBI) is a Standard conversion that occurred in October 2023. It is currently trading at 78% of book value. The average equity to assets the past two years is 12.8%; to be fair it was 8.8% in 2023. Home loans are 40% of their loans and another 32% commercial real estate. Non-performing assets was 0.14% last year and 0.29% in 2023.

SR Bancorp (SRBK) is a Standard conversion that occurred in September 2023. It is currently trading at 61% of book value. The average equity to assets for the past two years have been roughly 18%. ROE was negative in 2024, but they are releasing their 10-K in at the end of June. About 53% of their mortgages are home loans and I do not see any non-performing assets. In September 2024 they announced a 10% share buyback at around $12 per share.

Mercer Bancorp (MSBB) is a Standard conversion that occurred in July 2023. It is trading at 62% book value. The average equity to assets for the past two years have been roughly 13-15%. Non-performing assets were 0.21% in 2024 and 0.33% in 2023. ROEs have averaged 3.5% the past two years. NSTS Bancorp (NSTS) is a Standard conversion that occurred in January 2022. Last year they bought back 5% of its stock at an average price of $11.01; it is currently trading at $12.35. The stock is trading at 84% of book value. They also have 27% average equity to assets in 2024 and 30% in 2023.

VWF Bancorp (VWFB) is a Standard conversion that occurred in July 2022. The company is currently selling at 63% of book value. The average equity to assets for the past two years have been roughly 10%. Latest 10-K will come out at the end of June so I will buy a small stake and re-evaluate afterwards.

ECB Bancorp (ECBK) is a Standard conversion that occurred in July 2022. The stock is trading at 81% of book value. The company did a small stock repurchase in 2024 at $14.70 and in Q1 of 2025 at $14.58; looks like they bought back 1-2% of their shares combined. ROEs the past three years have been in the mid-2%’s.The average equity to assets for the past two years have been roughly 11-12%. About 60% of their deposits are CDs which isn’t great. Total non-performing assets to total assets are on average 0.12%.

Larry Seidman is a director at Bankwell Financial Group Inc (BWFG) and he was recently granted the right to increase his ownership from 10% to 15% of the company. The numbers below the hood look great; ROEs have averaged 12% for the past five years. The stock is trading at 102% of book value. As a whole the company has purchased 535,802 shares and this year they have repurchased 14,626 shares at a weighted average price of $28.86 per share.

Quotes & Charts

“You don’t have to do exceptional things to get exceptional results.” Warren Buffett

Napoleon on having a detective’s eye and noticing the details, even the invisible ones:

“All great events hang by a single thread. The clever man takes advantage of everything, neglects nothing that may give him some added opportunity; the less clever man, by neglecting one thing, sometimes misses everything.”

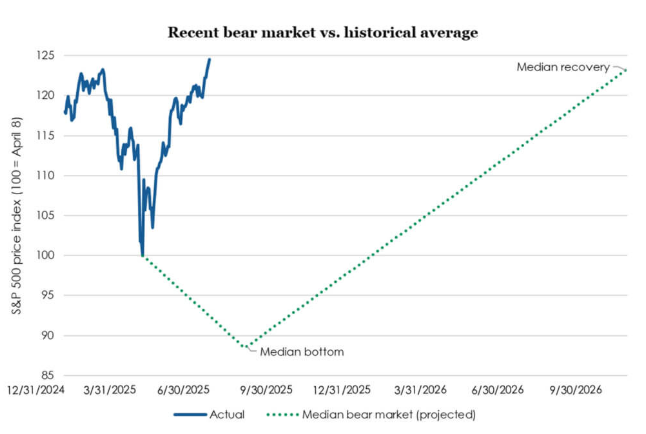

Trend following often struggles or lags during the initial phase of a bear market, but has historically provided significant diversification benefits during the prolonged grind down from -10% to the market trough.

Trend following managed futures are not a magic bullet against all market declines, especially the sharp, initial shocks. However, history suggests that during the longer, grinding phases of significant bear markets – the periods after the first 10% drop – trend following has often provided valuable, diversifying returns precisely when equity investors needed them most.

“Chart 3 shows the dividend yield/projected earnings growth combinations for selected equity groups. Groups in the “northeast” of the chart (i.e., higher yield and stronger growth) would be considered more attractive, whereas those in the “southwest” would be less attractive (lower yield and weaker growth).”

“The US and many global profits cycles are starting to decelerate, and the equity market segments that traditionally outperform when profits accelerate are typically not those that outperform when profits decelerate. Historically, quality has been a dominant factor when profits decelerate and, as the previous charts outlined, quality and defensiveness is currently undervalued relative to the popular Magnificent 7 and offers similar or even better growth than the Mag 7.”